by

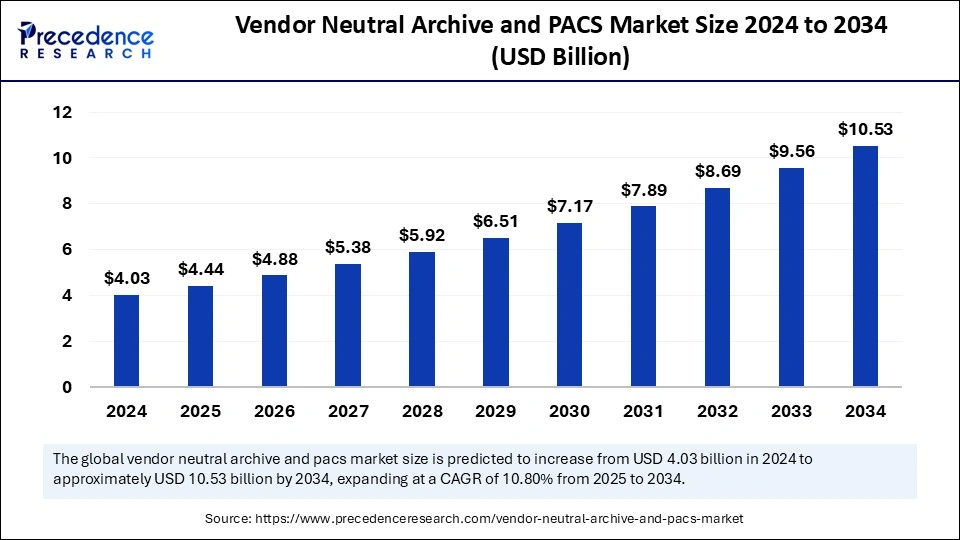

by The global vendor neutral archive and pacs market size is estimated to surpass around USD 10.53 billion by 2034 increasing from USD 4.03 billion in 2024, with a CAGR of 10.80%.

Get a Free Sample Copy of the Report@ https://www.precedenceresearch.com/sample/5772

Vendor Neutral Archive and PACS Market Key Insights

-

The North American region captured the largest share of the market in 2024.

-

Asia Pacific is projected to witness rapid growth from 2025 to 2034.

-

Among imaging modalities, computed tomography held the highest market share in 2024.

-

Magnetic resonance imaging is expected to grow at the fastest pace in the upcoming years.

-

Hospitals led the market as the primary end-users in 2024.

-

Diagnostic imaging centers are anticipated to experience strong market expansion in the coming years.

Role of Artificial Intelligence in the Vendor Neutral Archive (VNA) and PACS Market

Artificial Intelligence is transforming the vendor neutral archive (VNA) and picture archiving and communication systems (PACS) market by enhancing efficiency, automation, and diagnostic accuracy. AI-driven image analysis helps radiologists detect patterns and abnormalities in medical scans more quickly and accurately, reducing diagnostic errors and improving patient outcomes.

Machine learning algorithms assist in prioritizing urgent cases, automating image sorting, and generating reports, which streamlines workflow efficiency and reduces the administrative burden on healthcare professionals. Additionally, AI enhances data management by optimizing how medical images are stored, indexed, and retrieved, ensuring seamless interoperability across different healthcare systems.

AI also plays a crucial role in predictive analytics, cybersecurity, and cloud-based imaging solutions. AI-powered predictive models analyze imaging trends and patient histories to forecast disease progression and personalize treatment plans, leading to proactive healthcare interventions. Security mechanisms driven by AI help prevent unauthorized access, detect cyber threats, and ensure compliance with data privacy regulations like HIPAA and GDPR.

Furthermore, AI optimizes cloud-based PACS and VNA systems by improving bandwidth usage, accelerating image retrieval, and enabling real-time collaboration among healthcare providers. As AI continues to evolve, it is expected to further enhance medical imaging accuracy, streamline operations, and drive better patient care

Vendor Neutral Archive (VNA) and PACS Market Growth Factors

The increasing volume of medical imaging data is a key driver of the VNA and PACS market. With the rising prevalence of chronic diseases, advancements in imaging technology, and the growing adoption of digital healthcare solutions, healthcare facilities are generating vast amounts of imaging data. The need for efficient storage, retrieval, and management of these images is fueling demand for VNA and PACS solutions.

Additionally, the shift toward electronic health records (EHRs) and interoperability initiatives has further boosted adoption, as these systems enable seamless integration across multiple healthcare platforms, ensuring efficient access to patient data.

Another major growth factor is the increasing adoption of cloud-based VNA and PACS solutions. Cloud technology offers scalable storage, remote accessibility, and cost savings by reducing the need for on-premise infrastructure. The rise of artificial intelligence (AI) and machine learning in medical imaging is also enhancing the efficiency of these systems, allowing for automated image analysis, improved diagnostic accuracy, and streamlined workflows.

Moreover, regulatory compliance requirements, such as HIPAA and GDPR, are pushing healthcare providers to invest in secure and centralized data management solutions, further accelerating market growth.

Vendor Neutral Archive and PACS Market Scope

| Report Coverage | Details |

| Market Size by 2034 | USD 10.53 Billion |

| Market Size in 2025 | USD 4.44 Billion |

| Market Size in 2024 | USD 4.03 Billion |

| Market Growth Rate from 2025 to 2034 | CAGR of 10.80% |

| Dominating Region | North America |

| Fastest Growing Region | Asia Pacific |

| Base Year | 2024 |

| Forecast Period | 2025 to 2034 |

| Segments Covered | Imaging Modality, End-user, and Regions. |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Vendor Neutral Archive and PACS Market Dynamics

Market Drivers

A major driver of this market is the widespread adoption of digital imaging technologies. The transition from film-based radiology to cloud-based storage systems is improving workflow efficiency, reducing operational costs, and enabling remote access to patient data. Additionally, regulatory mandates promoting the use of standardized imaging systems further propel market growth.

Market Opportunities

AI and machine learning integration present significant opportunities in VNA and PACS. AI-powered image analysis, automated diagnostics, and predictive analytics enhance these systems’ capabilities, providing healthcare providers with more advanced imaging management tools.

Market Challenges

Data security concerns, high implementation costs, and interoperability issues between different healthcare systems pose significant challenges to the market. Healthcare providers must navigate these challenges to fully leverage VNA and PACS solutions.

Regional Outlook

North America leads the market due to its advanced healthcare infrastructure and regulatory compliance requirements. Meanwhile, Asia Pacific is expected to witness the fastest growth, driven by increased healthcare investments, digitalization of medical records, and the growing adoption of telemedicine solutions.

Vendor Neutral Archive and PACS Market Companies

- Merge Healthcare Inc.

- Visage Imaging

- Xerox Corporation

- GE Healthcare

- Caresyntax AG

- Canon Medical Systems

- Soft Imaging Systems

- Cerner Corporation

- Advanced Imaging Concepts

- Fujifilm Holdings Corporation

- McKesson Corporation

- Koninklijke Philips N.V.

- AGFA HealthCare N.V.

- Siemens AG

Leader’s Announcements

- In February 2024, FUJIFILM Healthcare Americas Corporation announced that its Synapse VNA and Synapse Radiology PACS solutions ranked #1 in the 2024 Best in KLAS Awards: Software and Services. This recognition, based on findings from KLAS Research, underscores the company’s achievement that significantly enhances patient care through its software and service offerings. Bill Lacy, senior vice president of medical informatics at FUJIFILM Healthcare Americas Corporation, said, “VNA is the core component to an effective Enterprise Imaging strategy, so we see this award as further validation of Fujifilm’s leadership position in the Enterprise Imaging industry.”

Vendor Neutral Archive and PACS Market Recent Developments

- In November 2023, Hyland Software, Inc. showcased its advanced diagnostic imaging and point-of-care technologies at this year’s RSNA conference. The company seeks to tackle healthcare challenges, such as workforce shortages and increasing demand, by providing solutions that enhance patient information and facilitate informed decision-making.

- In February 2023, Fujifilm Holdings Corporation declared its acquisition of Inspirata’s global digital pathology division, which includes the Dynamyx system. This acquisition bolsters Fujifilm’s healthcare capabilities, fostering collaboration among pathology, radiology, and oncology and enhancing integrated care delivery across the organization.

Segments Covered in the Report

By Imaging Modality

- X-Ray

- Computed Tomography

- Magnetic Resonance Imaging

- Ultrasound

- Nuclear Imaging

By End-user

- Hospitals

- Diagnostic Imaging Centers

- Ambulatory Surgical Centers

By Geography

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

Also Read: U.S. Patient Engagement Solutions Market

Ready for more? Dive into the full experience on our website@ https://www.precedenceresearch.com/

- Perishable Prepared Food Market Size to Attain USD 157.77 Bn by 2034 - April 24, 2025

- Fabric Filter Market Size to Attain USD 7.50 Billion by 2034 - April 24, 2025

- Pilot Training Market Size to Attain USD 31.38 Bn by 2034 - April 24, 2025